#11 Episode - A Framework for Venture Capital Fund Law

KEY TAKEAWAYS: Section 3(c)(1) venture funds have 100-beneficial owner limits (not 99!) plus any number of knowledgeable employees. Two parallel fund structures can be formed without integrating them. Each Section 3(c)(1) fund must be limited to 100 or 250 beneficial owners, unless it is a Section 3(c)(7) fund, in which case 1,999 Qualified Purchasers may join before the fund must be publicly listed.

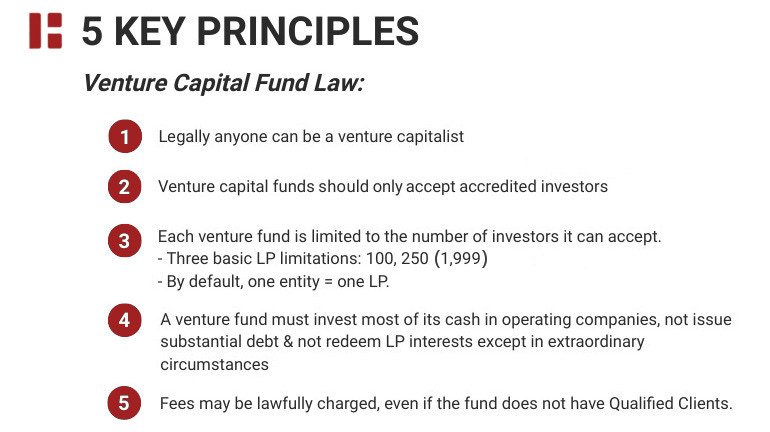

Venture capital fund law can be broken down into 5 Key Principles:

Venture capital fund law is a complex system of rules, regulations, and exemptions. But once you get the principles down, it’s not that difficult to understand the law.

John T. Reed wrote a brilliant passage about principles in Succeeding:

“When you first start to study a field, it seems like you have to memorize a zillion things. You don't. What you need is to identify the core principles – generally three to twelve of them – that govern the field. The million things you thought you had to memorize are simply various combinations of the core principles.”

Distilling complexity down to core principles accomplishes two things:

First, it shifts your mindset from information gathering to systems thinking. Systems thinking is about principles, patterns, and properties. A systems mindset allows us to process complex information in a systematic way.

Second, developing key principles compresses information for max distribution. Learning principles does not make you smarter or more of an expert. But it gives you a framework to spot patterns, understand structures, and with some time and experience, build mental models which can help you formulate unique solutions.

James Clear, author of Atomic Habits, recently shared a related idea in his newsletter:

To simplify before you understand the details is ignorance.

To simplify after you understand the details is genius.

And that sounded like Occam’s Razor, a principle summarized as follows:

Entities should not be multiplied without necessity.

In other words, the simplest explanation is preferable to one that is more complex.

This concept is illustrated by Dr. Seuss’ Cat in the Hat Comes Back children’s book:

The story centers on a mischievous cat who wears a tall red and white-striped hat and a bow tie. The Cat in the Hat shows up at the house of Sally and her brother while their mother is away. The Cat runs into the house uninvited, hops into their bathtub and eats some cake. He leaves a pink stain in the bathtub. The pink stain spreads throughout the house as the children try to remove it, until the Cat comes up with a solution (actually, about two dozen solutions—under his hat!).

“I can clean up these rug spots

Before you count to three!

No spots are too hard

For a Hat Cat like me!”

The only problem is that the Cat can’t deliver on his promise. He needs backup:

But the cat just stood still.

He just looked at the bed.

“This is not the right kind of a bed,” the cat said

“To take spots off this bed will be hard,” said the cat.

“I can't do it alone,” said the Cat in the Hat.

The Cat then summons smaller cats named A through Z who are hiding underneath his hat to help him fix their intractable pink-stain problem. After dozens of unsuccessful attempts, the story ends with Little Cat Z, who creates enough suction (VOOM!) to remove all the pink from the property. Case closed.

Some takeaways from this 1950s children’s story:

Be careful about accepting unsolicited advice or unwelcome help from strangers, particularly from those who got you into a situation in the first place;

“If you want something done right, do it yourself” (Napoleon); and

Map out your problem and solutions, anticipate which ones are clearly bad before blindly taking unnecessary steps (see, e.g., Balaji Srinivasan’s “Idea Maze”).

Everyone knows that E = mc². The key insight for us is not in the math formula itself, but in the power of its compression:

Everything should be made as simple as possible, but no simpler. —Albert Einstein

The Five Key Principles

Let’s try to unpack the five key principles simply, without creating a mess.

#1: Legally Anyone Can Be a VC

Venture capitalists file and maintain a form called a “Form ADV” to comply with their Exempt Reporting Adviser (“ERA”) obligations. In plain English, VCs receive special treatment. They operate without a license. To avoid all the rules and regulations of a registered adviser, they just have to follow through on some disclosure forms.

[Edit: 10/29/2020] In addition, the SEC just amended its accredited investor rules to allow certain investors to participate in the fundraising of private funds regardless of wealth as a sole proxy for financial sophistication. These new rules take effect on December 8th, 2020.

[Edit: 10/29/2020] Here are the two best kept secrets from the new securities rules:

First, a non-accredited investor can become an accredited investor simply by raising a fund with at least $5 million in “investments” (as defined in Rule 2a51-1(b) under the Investment Company Act), provided the fund is not itself formed for the specific purpose of acquiring the securities being offered. Rule 501(a)(9).

Second, “Knowledgeable Employees” will not disqualify a fund’s accredited investor status even if the fund has less than $5 million in assets, per Rule 501(a)(11).

In fact, it’s surprising to me how little regulation is involved in venture capital. VCs can literally raise and invest millions of dollars of other people’s money without needing a license, a college degree or even a passing grade on an entrance exam.

By contrast, for example, the Board of Barbering & Cosmetology of California requires hairdressers to have: (i) a high school diploma, (ii) 1,600+ hours of school (2x for apprenticeships), (iii) written & practical exams, and (iv) a cosmetology license, not to mention the significant health & safety procedures they must follow in a pandemic.

In theory, anyone can be a VC; but in practice, it’s more insular than people think.

In 2018, Richard Kerby, a GP at Equal Ventures, found that ~40% of all VCs hail from two educational institutions, while 82% are male and 60% white male.

A recent study by Women in VC found that only 4.9% of VC partners are women, with 33% of those being women of color. Less than half (or 2.4%) are founding partners. Nearly 90% of women-led funds are “emerging fund managers,” with 73% founded in just the past five years, 23% currently raising their first fund, and 44% are deploying it.

In 2020, however, things are looking different. Dozens of diverse emerging fund managers launched their rolling funds on AngelList. Calls for diversity on cap tables have never been higher. And there have been key announcements from trail-blazing fund managers like McKeever Conwell at RareBreed Ventures, or Kara Nortman, who, on Monday was named Co-Managing Partner of Upfront Ventures, a $2 billion LA-based venture firm.

#2: VC funds should only accept accredited investors

Rule 501 of Regulation D defines accredited investors as:

Individuals: who have (i) a [joint] net worth of at least $1 million (excluding primary residence); or (ii) annual income of $200,000+ ($300,000+ with spouse or “spousal equivalent”—generally, "a cohabitant occupying a relationship generally equivalent to that of a spouse"), and

Entities: who have total assets of at least $5 million; or, the entity is owned exclusively by all accredited investors.

It’s best practice to reject non-accredited investors in a venture capital fund. Investment time horizons are typically a decade or longer. Coupled with the fact that, unlike a startup, venture funds cannot offer redemption rights, and GPs and emerging fund managers would be wise to consider steering clear of non-accredited investors.

[Edit: 10/29/2020] Here’s the graph that proves why you should not to allow non-accredited investors in your venture capital fund:

(To highlight the point, 0% of VCs have reported at least one non-accredited investor in their offering, ~1% of VCs indicate they might accept non-accredited investors).

[Edit: The SEC found that between 2009 and 2019, only between 3.4% and 6.9% of the offerings conducted under Rule 506(b) included non-accredited investors.]

So, while it might be theoretically possible to have non-accredited investors in a fund, advertising or solicitation would be prohibited. Plus, another major concern is integration. If the venture fund accepts money from non-accredited investors, any earlier or subsequent offering might be integrated with the current offering and put the entire fundraising process into jeopardy.

There are two caveats to accepting only accredited investors:

First, “Knowledgeable Employees” can lawfully invest in the venture fund they work for under new Rule 501(a)(11). Importantly, these employees will not count against the 100 investor limitations under Section 3(c)(1). We previously discussed this rule which goes into effect on December 8th, 2020, but here’s a quick refresher:

Employees must be participating in the investment activities of the fund—and not solely clerical, secretarial or admin tasks—for 12+ months.

The “12 month” requirement for Knowledgeable Employees can be “on behalf of another company for at least 12 months”

Executive officers, directors, general partners, and persons serving in a similar capacity of a venture capital fund will count not only as “accredited investors” per Rule 501(a)(4), but under the new rules, they may also qualify as “Knowledgeable Employees” per Rule 501(a)(11).

This has two important implications.

First, under Rule 501(a)(8), a private fund with <$5 million in assets may qualify as an accredited investor for purposes of investing in startups so long as all of the equity owners are accredited investors—“Knowledgeable Employees” are considered accredited investors per new Rule 501(a)(11).

More importantly, “Knowledgeable Employees” do not count against the 100 person limitation set forth in Section 3(c)(1) of the Investment Company Act. This applies not just to employees themselves, but to the core investment team, including the GPs, VCs and other decision makers.

KEY TAKEAWAY: The key investor limitation of Section 3(c)(1) venture funds is not 99 LPs but 100-beneficial owners plus any number of knowledgeable employees.

Which brings us to the next principle: Understanding LP Limitations.

#3: Understanding LP Limitations and their Exceptions

Elizabeth Yin of Hustle Fund started a great Twitter exchange by asking a simple, but insightful question:

I spent some time going through the Congressional record to see if there was any stated policy or rationale for why investor limitations were limited to 100 (please note I believe it’s 100 beneficial owners, not 99). The answer appears to be a combination of “we know it when we see it” arbitrary rationale and Dunbar’s number.

Here’s a quote from Marianne Smythe, a former SEC Commissioner, delivering her research to Congress on the legislative history of the Investment Company Act of 1940:

The legislative history of section 3(c)(1) indicates that the 100 investor limit represents an outer limit of an investor base likely to be composed of people with personal, familial, or similar ties. In some circumstances, investor protection concerns may be raised by small investment pools whose securities are held by investors of modest means, even if the pools have fewer than 100 investors. But the concept that the investors in these smaller pools are bound by personal or familial ties retains some validity, and, in any case, federal oversight of these pools under the Investment Company Act would be impractical.

[In summary,] the 100 investor limit is an effective proxy for requiring that the investors have some relationship outside the pool, such as familial or social ties.

—Protecting Investors: A Half Century of Investment Company Regulation (1992) by the Securities and Exchange Commission.

Beneficial Owners under Section 3(c)(1)

There are two relevant statutes for venture capital funds.

The first statute is Section 3(c)(1) of the Company Act:

There are two key elements under Section 3(c)(1):

A 3(c)(1) fund is limited to 100 beneficial owners (250 if fund <$10M)*; and

It cannot be “making or proposing to make a public offering of its securities.”

The first element limits the number of beneficial owners of a fund’s outstanding securities to no more than one hundred persons (or, in the case of a “qualifying venture capital fund” with less than $10 million in aggregate capital contributions and uncalled capital commitments, 250 persons).

That second element may be a bit confusing given that Rule 506(c) of Regulation D allows solicitations. At first blush, people seemed to have an issue with the Rolling Venture Fund product precisely because the plain language of the statute suggested you couldn’t make a public offering. But Congress made it clear that wasn’t the case:

The JOBS Act also added new Section 4(b) to the Securities Act (15 U.S.C. § 77d(b)), which provides that offers and sales exempt under Rule 506 “shall not be deemed public offerings under the Federal securities laws as a result of general advertising or general solicitation.”

Here’s the default rule for counting investors as part of the 100 (or 250 if under $10 million) beneficial owner limitations under Section 3(c)(1) funds:

In other words, by default:

One Entity = One LP.

Qualified Purchasers under Section 3(c)(7)

The other relevant statute for VC funds is Section 3(c)(7) of the Company Act.

Section 3(c)(7) exempts the fund adviser if the adviser only accepts “qualified purchasers,” as defined in Section 2(a)(51) of the Company Act, to his fund.

Qualified purchasers include (A) natural persons and family-owned businesses or individuals who own at least $5 million in investments, or entities and trusts if they own and invest a minimum of $25 million in investments.

Section 12(g) of the Exchange Act prevents Section 3(c)(7) funds from becoming larger than 1,999 LPs without them subject to public registration rules.

Here are two more key takeaways:

KEY TAKEAWAY: You can create two parallel fund structures to match the Section 3(c)(1) fund with the Section 3(c)(7) fund and they will not integrate together.

For example, the SEC staff has stated that similar funds with the same general partner may be “integrated” (viewed as a single fund) for purposes of the 100 beneficial owner limit of unless a reasonable investor would consider interests in the two funds to be materially different. A fund relying on Section 3(c)(1) will not be integrated with a fund relying on Section 3(c)(7), provided that qualified purchasers are only accepted by the latter fund.

KEY TAKEAWAY: The 1,999 limitation is only a trigger to force the company to go public. It’s not a true limitation in the real sense of the word. Rather it acts like a buffer or alarm before the fund must go public.

Under Section 12(g) of the Exchange Act, a company is required to register a class of equity securities under the Exchange Act if it has more than $10 million of total assets and the securities are “held of record” by either 2,000 persons or 500 persons who are not accredited investors.

Look Through Rules

There are basically four exceptions to the default rule of counting 1:1 ratio of LPs-to-Beneficial Owners:

#1: An LP invests 10% or more of the voting interests* of the fund.

#2: An LP invests 40% or more of the LP’s assets.

#3: An LP creates an entity for the specific purpose of investing in the fund.

#4: Section 48(a) of the Company Act generally makes it unlawful for any person to do indirectly through another person or entity what would be unlawful for the person to do directly and it gives the SEC the authority to "look-through" a transaction if it is a sham or conduit formed or operated for no purpose other than circumventing the requirements of the Act.

*limited partnership interests are almost always considered voting securities even if the voting is limited to a supermajority right to replace the GP.

There are a lot of ways to illustrate the Look Through Rules but this question was asked recently and it seemed like a good one to illustrate the concept.

Q: Can SPVs invest in a venture capital fund if they invest 10%+ in the fund or were formed for the specific purpose of investing in that fund?

A: Generally, yes, but you have to count all of the beneficial owners behind that LP as part of the 100 beneficial owner limits under Section 3(c)(1) (assuming the investors are not qualified purchasers or have not been exclusively placed into a separate Section 3(c)(7) fund where at least one investor is not a qualified purchaser).

Subscription documents will often include reps & warranties that disallow SPVs formed for a specific purpose. Cooley, Gunderson & Wilson all have docs with this blanket prohibition. For example, here’s a quote from a subscription agreement:

If the Subscriber is not a natural person, the Subscriber represents and warrants that …. (iii) was not organized for the specific purpose of acquiring the Fund Interest.

By default:

• One Entity = One LP (Section 3(c)(1)(A)).

But if the SPV was formed for the specific purpose of investing in a fund, the beneficial ownership should be that of the “holders of such company’s outstanding securities (other than short-term paper) will count”. In other words, count all the number of people who stand to make money (spouses do not count as separate investors).

Any answer should utilize the "Look Through Rules" to count the total number of beneficial owners.

#4: Invest in Equity, No Substantial Debt & No Redemption Rights

A venture capital fund is a special type of private fund that*:

✅ holds itself out as pursuing a venture capital strategy;

✅ holds at least 80% of its assets in “qualifying investments” or cash;

✅ is not substantially leveraged;

✅ does not provide redemption rights except in extraordinary circumstances; and

✅ is not registered under the Investment Company Act.

Some key differences of venture capital funds compared to other types of private funds:

Venture capital fund advisers get their own exemption—whereas hedge funds, private equity funds, crypto funds, etc. are all lumped together as “private funds”.

Venture capital fund advisers may not legally hold more than 20% of capital in anything outside of cash or equity securities issued directly by portfolio companies.

Venture capitalists are limited when taking loans or issuing more than 15% of debt—whereas private equity funds usually take out as much debt as possible. VCs have maximum leverage limits and even then require outstanding loans to be repaid within 120 days of borrowing. Banking becomes a lot more interesting.

VC funds can’t offer redemption rights, except in extraordinary circumstances.

VC funds can raise an unlimited amount of capital without having to register with the SEC; on the other hand, private funds must generally register with the SEC once their regulated assets under management hits $150 million.

#5: Fees may be charged even if the fund has no Qualified Clients

Venture capital fund law is fairly straightforward because the SEC affords VC fund managers special legal status by providing them with an exemption named after them—“Venture Capital Fund Adviser Exemption.”

Generally, ERAs are investment advisers that rely on either the Venture Capital Fund Adviser Exemption (Section 203(l)) or the Private Fund Adviser Exemption (Section 203(m)).

There are several reasons why compliance for VCs is easier than other private funds. One of the major benefits of being a venture capital fund adviser as opposed to another kind of manager is that you don’t have to worry about charging performance fees to LPs:

Because exempt reporting advisers (ERAs) are not registered with the SEC, the prohibition on performance fees contained in Section 205(a) of the Advisers Act does not apply.

—Concept Release on Harmonization of Securities Offering (2019), p. 182.

Subscribing to the Law of VC newsletter is free and simple. 🙌

If you've already subscribed, thank you so much—I appreciate it! 🙏

As always, if you'd like to drop me a note, you can email me at chris@harveyesq.com, reach me at my law firm’s website or find me on Twitter at @chrisharveyesq.

Thanks,

Chris Harvey