#12 Episode - The Un-American Rule

Legal Fees: Not a Hill to Die On, But Some Parity Would be Nice

Most industries have unwritten rules that are shocking when you first learn of them. Often, these rules are so widespread that they become calcified and beyond negotiation. Today, we focus on such an unwritten rule in venture capital—legal fees.

Background on Legal Fees

In courtrooms all across the United States, litigants follow ‘The American Rule’—that is, each party is responsible for paying for their own legal counsel unless (a) there is a specific law that authorizes fees, or (b) the contract includes an attorneys’ fees clause.

The VC industry does not follow the American Rule. The unwritten rule is founders must pay for their own attorneys’ fees, plus their VC’s legal fees, up to a negotiated cap.

Nothing is Standard in Venture Capital

Fee shifting is so pervasive in this industry that it’s often said to be “a standard term” in negotiations. (Remember Morty’s words: Nothing is standard in venture capital).

People will often use this line to justify terms favorable to them. Can you think of a single time when someone opposite of your position told you “this is a standard term” and it benefited you or your client? If not, then how can we seriously treat this as a standard term? But even if it was a standard term, is it fair and reasonable?

My Fee Shifting Story

A couple of years ago I had an eye-opening experience with this fee shifting norm. My client was a budding startup looking to close a $2 million Seed investment from a publicly-traded corporation. It was the investor’s first attempt at corporate venture capital. They wanted it done right so they hired a top law firm out of Silicon Valley.

IPO Deal Team

The only problem was that the deal team they picked also happened to be the same deal team that took the company public. It was an elite group of highly-skilled IPO lawyers who practiced in the public markets, helping clients file their S-1s, doing public due diligence and doing all things necessary to get a company to go public. A difficult job, to be sure, but not exactly related to early-stage investing.

This was also not a cheap bunch of lawyers. The partner charged $1,200 per hour, senior associates ~$900 per hour, and the first and second year associates ~$550+ per hour. $2 million was probably an average legal fee for them on an IPO deal.

By comparison, the top quartile hourly fees charged by corporate attorneys with 10+ years of experience is $450 per hour. A lightweight Series Seed deal should cost between $5K and $15K+, an average fee cap is $20K, whereas a heavier-Seed or Series A deal ranges typically between $30K and $65K+. (Bloomberg Law: Survey of 140+ startups; see also Aumni/NVCA Term Sheet).

Series Seed Forms or NVCA Preferred Stock documents

On our initial kickoff call, the topic of “what legal forms should we use?” came up. Given that it was a light-to-normal Series Seed deal, I suggested Series Seed documents, originally drafted by Ted Wang/Jason Boehmig while at Fenwick. The lead attorney (let’s call him Frank) disagreed.

Frank: “You mean Series Seed DOT COM documents?” he said. “What are you talking about? Those forms haven't been used around here for over 10 years.”

I explained to Frank that Series Seed “dot com” documents were common for light-to-normal Series Seed deals, including in Silicon Valley today (I had the tweets to prove it!) Frank would hear none of it. To Frank, there was only one option: NVCA forms.

I said, “Frank, if we are going to use the NVCA documents, that's fine, but we will end up spending 3x more in legal fees.” I sent him guides and articles explaining this and even backed it up with anecdotal evidence.

I left Frank with this quote from Fenwick & West:

The full Series A documentation is typically significantly more expensive in legal fees, and requires the negotiation of all the terms and documents that will be used in a later Series A financing. This can be difficult since the seed round often does not include traditional lead investors with which the company can negotiate the documents. This structure of transaction can typically take four to six weeks to complete (from finalization of the term sheet to closing of the investment). —Fenwick & West, Seed Financing Overview

Frank again disagreed and so I made him an offer: If his client promised that it would charge no more than $15K in attorneys’ fees, then we would agree to use the NVCA forms. Frank agreed, but on the condition that we draft the forms.

Although we had secured a legally enforceable right that no more than $15K in attorneys’ fees would be charged to my client, it didn’t matter. True to form, the IPO deal team ran a heavy due diligence over the next six weeks and amassed a six-figure legal fee. To get the deal done, my client was told it had to cover at least half the deal team’s fee, at which this point was well over six figures. They said the “$15K was a mistake” and the “spirit of the deal was always to cover half of our legal fees.” What’s ironic was that we had only one enforceable term in the term sheet and it was the $15K fee cap.

My client conceded. In the end, Frank got what he wanted and his multi-billion dollar client was more than happy it passed along the costs to my client, the startup that actually needed the funds.

Some time later, after reflecting on the turn of events and the bad taste it left me, I ended up tweeting this out (unfortunately, the real amounts were much higher):

Standard Legal Fees

Obviously, what happened wasn't fair and it’s been a far outlier from my experience. However, it laid bare the power that VCs and their fund counsel have when compared to founders who either don’t know about or don’t have the leverage to negotiate.

There are essentially three camps of how you might view attorneys’ fees clauses in the context of venture capital financings:

Camp #1: You See like a Venture Capitalist

All venture capitalists are on an annual budget. A lot of people think that VCs have a lot of money to spend on legal fees and miscellaneous expenses. While that might be true at a multi-stage, top tier venture capital fund with in-house counsel and management fees that have stacked up over the years, it’s not true for most VCs. And it’s certainly not true for emerging fund managers who haven’t raised beyond their second or third fund, and for those who have only raised $50 million or less.

For most emerging fund managers, every dollar counts.

Fund managers also don’t think it’s unfair that founders shoulder some of the burden—because it gives the manager the ability to operate without having to ask for more management fees, which can be seen as a misalignment of interests with their LPs.

Camp #2: You Understand Both Sides, But You Recognize There’s Bigger Fish to Fry

This camp understands there is a misalignment of interests between founders and venture capitalists and that VCs typically have the power in this imbalance. But when it comes to legal fees, these are necessary costs to get deals done. Standard forms can help mitigate costs, as can legaltech. But in the overall context of venture capital, legal fees are just the cost of doing business. We shouldn’t sweat the small stuff because it gets in the way of important things like company building and venture scaling. Negotiate a cap and stick to it.

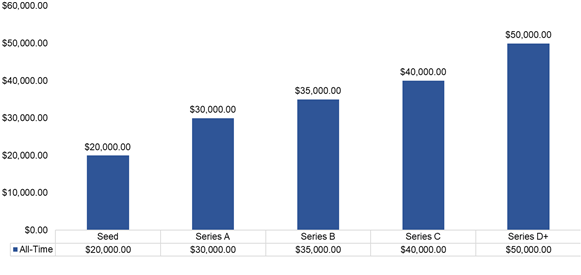

There is a standard set of legal fees that the venture capital industry follows. It’s a step function for each financing round (chart taken from Aumni’s Enhanced Term Sheet):

Investor Counsel Fee Cap Across Stage

As someone wrote on Twitter recently, “it’s strange how legal fees are just under the cap or way over the cap with copious discounts, but we never see legal fees significantly under.” Given the amount of legal work it should take to get a deal done, it’s an unfortunate, but true cost. Without legaltech, that’s true.

The legal industry is fixated on hourly rates or flat fees with higher than average costs because there hasn’t been a strong push to drive those costs down. First, I don’t think a big law firm model would support lower costs. Second, there are legaltech tools that already help mitigate this, but there isn’t an industry standard. Not yet anyways.

Camp #3: You Are a Founder-Friendly Empath

As a former founder or someone who empathizes with their lot, you think that startups paying for their VC’s attorneys’ fees is hogwash.

Camp #3 believes venture capital funds have the ability to pay for their own expenses, so they should cover their own legal fees. VCs already pay for things like back office fund administration, fund formation fees, operations, accounting, and audit fees. There is no reason these funds can’t also pay for their own legal expenses.

This camp reminds me of a recent story that Dave Portnoy, founder of Barstool Sports, told to Anthony Pompliano on the Pomp Podcast about a similar experience he faced:

“I remember the Chernin [Group] deal. There was like $50,000 in lawyer fees that I know at the beginning they [promised to] cover my lawyer fees. It’s $50,000. It was a lot of money for me at the time. And we were at the last moment of the deal and they said ‘Yeah, you pay for our lawyer fees.’ And I said no, we agreed that you did. They tried to renegotiate it. And I literally said at the end—I’m like—‘the deal is off.’ They offered $40,000, not $50,000. And I said, ‘It’s $50K or the deal is off because we agreed on it.’ If we agree on something with me, you better fucking honor it, or I will walk.”

Conclusion

There are a few VCs in the industry that do not follow the unwritten rules of venture capital, but follow the American Rule instead. These VCs understand the costs that startups face and have undertaken to either completely waive their attorneys’ fees or set a floor before fees kick in—in other words, if the parties go over a certain agreed-upon threshold ($20K-30K, for example), then the startup pays for or splits those costs above that threshold amount.

Here are the VC funds that fall into the latter camp:

Street*

*If your venture capital firm does not charge its founders attorneys fees, please reach out to me as I will update this article over time.

Last Updated August 17th, 2021.

Subscribing to the Law of VC newsletter is free and simple. 🙌

If you've already subscribed, thank you so much—I appreciate it! 🙏

As always, if you'd like to drop me a note, you can email me at chris@harveyesq.com, reach me at my law firm’s website or find me on Twitter at @chrisharveyesq.

Thanks,

Chris Harvey

Hi Chris, really enjoying the series of articles. My understanding for the startup picking up the tab was so that the lead firm didn’t just get stuck with the bill with other investors riding on their coat tales, which kind of makes sense. My experience is that fees go sideways when the startup docs/structure/ records are in a bad way and need to be cleaned up. Fixing ‘legal technical debt’ is often 10x the cost of doing it right in the first place. Cheers Toby