#2 Episode - Rolling Venture Funds through the Good Times and the Bad

AngelList's Rolling Venture Funds model + legal structure

KEY TAKEAWAY: A rolling fund is a new type of venture capital fund structure that allows fund managers to create new funds on a quarterly subscription basis.

On February 5, 2020, just before our world was upended by a global pandemic, AngelList announced its Rolling Venture Funds program. Alex Konrad wrote a great piece about the launch. It earned social media attention, even receiving a retweet from me ("Amazing!”). But then, the pandemic hit, and we forgot about it.

Renewed interest surfaced in July 2020 when Cindy Bi retweeted Alex's original article. She called the model "genius". By early August 2020, ~15 new fund managers were already launching their own Rolling Venture Funds on AngelList.

VC Twitter reacted with 🔥:

But not all the feedback was 😍. Some reactions on Twitter were 😕, 🤔 & even 🤨.

“I don’t believe this is legal.”

“How is this not solicitation?”

“[I]n my experience, every lawyer I’ve spoken to has advised against this due to liability but happy to say I was wrong on legality.”

Background

So, what are Rolling Venture Funds, what’s their legal structure and is any of this legal?

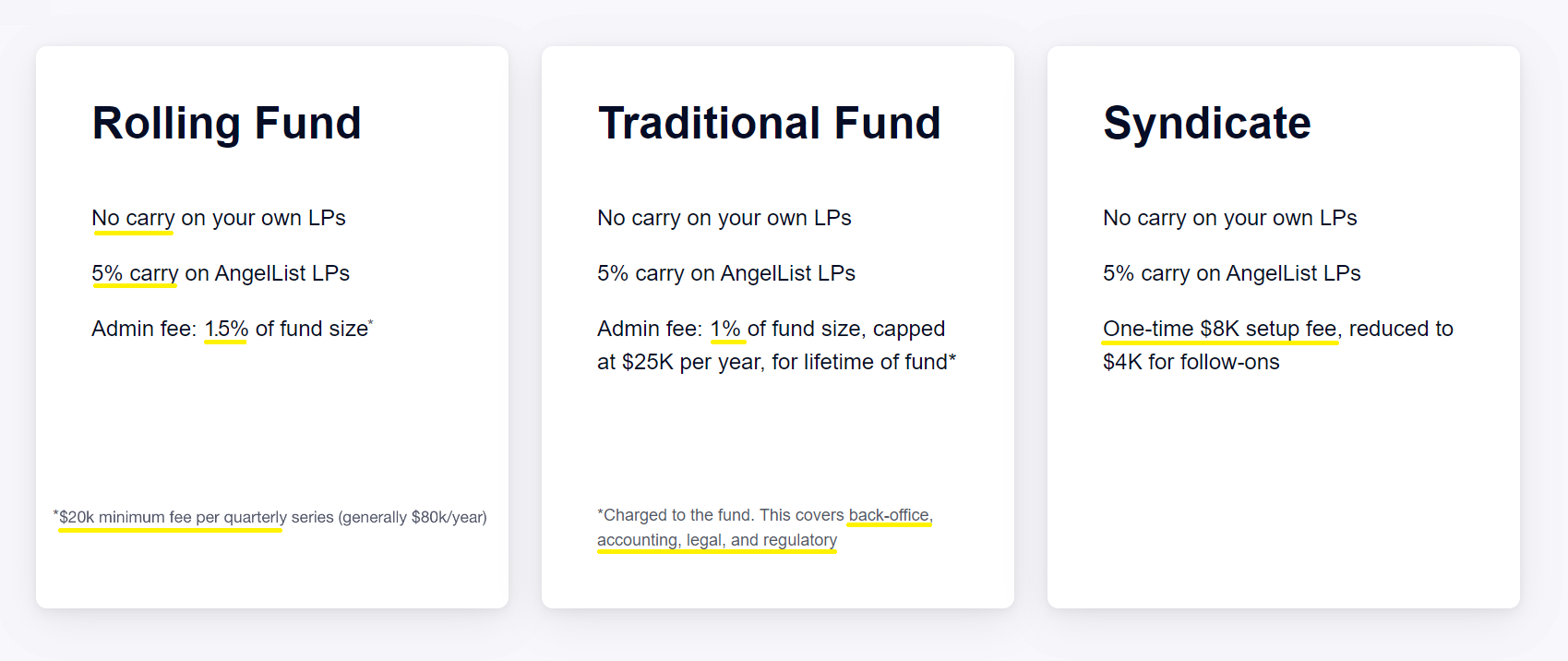

Rolling Venture Funds is one of three products that AngelList offers to fund managers:

Rolling Venture Funds (est. 2020)

Traditional Venture Funds (2017)

Syndicates—which are really just SPVs (2013)

A rolling fund is structured as a series of Delaware limited partnerships: capital commitments are open for an initial period and close when manager is ready to deploy capital. Each quarter, a new fund is offered on substantially the same terms as the previous quarterly fund, for as long as the rolling fund continues to operate. With this fund structure, rolling funds are publicly marketable and remain open to new investors. (Hence the term, “rolling.”)

1. Economics

At manager’s discretion. Most are charging industry standard “2 and 20” fee structures—but this can vary. For example, management fees can be saved, reinvested or waived at the emerging fund manager’s (“GP’s”) discretion.

Management fees: ~2% per year, calculated and charged quarterly

Carry: 20%, more if certain threshold is reached (e.g., 1–3x fund multiple returned)

Recycle fees: A fund manager will reinvest a portion of the management fees back into their fund, which lowers the total effective cost

Minimum term commitment: Single quarter to four or more years

AngelList charges the Fund Manager:

Platform admin fee: “0.15% of capital commitments per year, charged over 10 years”

[EDIT: 9/3/20 AngelList revised its marketing but the pricing has not changed - for each new fund, the fees are 1.5% of committed capital on a quarterly basis, payable over 10 years, or 0.15% per year]—this should cover Delaware annual franchise fees ($300/yr) plus state franchise taxes in places like California ($800/yr). Fees such as agent for service of process, annual state reporting, back office costs, etc. should also be covered by AngelList

The minimums say $20K per quarterly fund, which if you do the math it can render some high fees (1.5% of a $1 million fund = $15K, but $20K per quarter is $80K per year, which over a ten year basis is ~$800K in fees)

The truth is that AngelList is providing a great service for the price you pay, but if you continue to rely on the service, those fees will stack and grow over time. For example, let’s assume you raise $4 million over 4 quarters (4 Rolling funds with $1 million in each Rolling Fund).

First quarter’s fees (no minimums): 1.50% x $1 million = $15k/10 years/4 quarters = $375 (nothing!)

Second quarter’s fees (no minimums): 1.50% x $1 million = $15k/10 years/4 quarters = $375 + $375 = $750 (next to nothing!)

Third quarter’s fees ($20k minimums): 1.50% x $1 million = $15k, but minimum fees are $20k, so $500. $375 + $375 + $500 = $1,250 (still almost nothing, but growing).

Fourth quarter’s fees ($20k minimums): 1.50% x $1 million = $15k, but minimum fees are $20k, so $500. $375 + $375 + $500 + $500 = $1,750 (this is when we start to see the steady climb of fees).

If we stopped there, there would be a total of ~$70,000 in AngelList platform fees over 10 years, for $4 million raised, which would equal 1.75% of AUM (the amount raised). And it would equal more than this if you stayed with the platform for more than a year (for 10 years, it would cost you $800,000 at a minimum). This is on top of the management fees. Still this is not a lot of admin fees and this is paid over time, but if we continued with the program, those fees would continue climbing until they reached a much higher percentage.

Carry: 0% if LPs are sourced by GP; 5% if LPs are sourced by AngelList

2. Key Differences

Each product offering operates under a similar legal structure. Rolling Venture Funds can be setup to look like a Traditional Fund structure, but the reverse is not true. Rolling Funds are unique in that (1) GPs can accept capital anytime, (2) GPs can deploy capital immediately, (3) LPs can auto-subscribe to the fund like a SaaS product for as little as $1,000 per fiscal quarter (again, at the GP’s discretion)

3. Who’s This Product For?

Rolling Funds allow people to “turn their reputations into investing capital,” as Leo Polovets (@lpolovets) wrote:

“If you're a principal at a larger venture fund that doesn't have near-term partner openings, (or you’re a VC-backed operator with cred like @shl) and you have 10k+ Twitter followers, why wouldn't you spin out to do a rolling fund? You can advertise your fund publicly, leverage your audience, and accelerate your career.

Legal Structure

AngelList uses a relatively new type of entity structure in Delaware called the "Series Limited Partnership" (“Series LPs”). The Series LP works like Matryoshka dolls:

"Matryoshka" is a traditional set of Russian dolls. Hidden inside the largest doll is a smaller doll. And inside the smaller doll is another doll, and so on.

The top Matryoshka doll is the Master Limited Partnership (“Master LP”). Underneath the Master LP are any number of sub-funds—Series LPs—that can be spun out of the Master LP. Funds can be created in a recursive, contractual loop without having to file new entity paperwork each time in Delaware (complications may arise—e.g., you may need to register the LP as a foreign entity in the manager's home state):

“The series fund concept is useful because it permits the formation of only one legal entity. For example, a series mutual fund formed as a legal entity under state law has only one board of [managers], one set of officers, etc. It files a single registration under the Investment Company Act of 1940. The use of the series is thus designed to save expenses for the fund’s interest holders.” —Humphreys, Limited Liability Companies § 1.04 (Revised 2006).

AngelList forms a new and distinct Series LP fund each quarter. The process is repeated for however long the GP is actively investing.

Each Series LP has a lifespan of 10 years + 2 years, if the term is extended by the GP’s option.

AngelList’s in house legal team will make tweaks to the Limited Partnership Agreement (“LPA”) on a case-by-case basis. It will also help prepare the GP’s required Exempt Investment Adviser form.

Note: The Fund Group at Wilson Sonsini “vetted” the above legal structure.

AngelList hired Belltower Fund Group to act as the fund’s administrator, managing back office functions including accounting, tax reports and LP ledger. AngelList acts as the fund’s Investment Adviser working alongside the fund managers to ensure the LPs are treated fairly and in a consistent manner. This can take the form of checking for conflicts, verifying information, and ensuring that all laws and regulations are complied with.

Issues with the Rolling Funds Model

As noted above, not everyone is convinced the Rolling Venture Funds model works. Excellent issues were raised by Ali Hamed on Medium and others users on Twitter:

1. General Solicitation

Some people argued that general solicitation is not permitted when raising funds. But under U.S. securities law Rule 506(c), fund managers are permitted to advertise their offering to the public. The caveat is the fund must take “reasonable steps to verify” each LP is an accredited investor. However, Rolling Venture Funds do not need to be launched under Rule 506(c)—they can use Rule 506(b), which is a common private exemption that does not allow general solicitations. And it should be noted that some states (such as New York) have additional disclosure laws and tax codes that may be necessary to comply with.

2. Carry Calculations

Quoting from Ali Hamed’s Medium post:

“But in the case of a rolling fund, you could invest $100k, lose 30% of your money, and the GP could still get carry. How? The fact that each vintage is its own distinct entity means that the carry on each deal is cross-collateralized. And therefore if one deal flops, it won’t wipe out part of the carry from the next winner.”

Avlok Kohli, the CEO of AngelList, clarified that carried interest is cross-collateralized across two years of fund cycles (up to 8 separate vintages).

3. Reporting

It’s uncertain as to how AngelList will accurately record fund metrics like IRR or address portfolio fund construction, but with the combination of risk exposures and different LPs stacked in the process, it will either make for a good or bad use case of the Series LP model. Avlok writes that AngelList has a “deep infra[structure] and software for reporting.”

4. Allocations

As Ali Hamed wrote, there may be some issues with allocating capital across funds:

“It’s really hard for VCs of any size or merit to get exactly their perfect allocation each time. Even the best firms like First Round or Floodgate don’t do this perfectly. So odds are, there is going to be either too much demand for deals, or too much capital, leaving excess cash in the vintage. What happens to that cash?”

But Rolling Venture Funds are like Rollover Data plans with cell phone carriers. Any unused capital during the quarter will “rollover” to the next quarter. Capital commitments will continue to stack up until turned off by the LP or GP.

5. Pro Rata Decisions

Finally, Ali Hamed was concerned about how GPs will make pro rata decisions. Avlok suggested to spin-up SPVs and offer LPs one-time opportunities on a per-deal basis. Structural changes could be made in the LPA to add, for example, a right of refusal so that every LP can participate in the fund chain. This is a more complicated issue. Definitely something fund managers should consider before committing.

6. Key Person and Successors

Other users on Twitter pointed out Key Person and Successor issues—what happens if the fund manager commits fraud or misappropriates funds during the investment period? What recourse do LPs have against the manager or AngelList? As referenced above, AngelList is an investment adviser to each fund. If a GP materially violates the LPA then AngelList has control rights. So there is some authority overlooking the fund managers.

7. No Getting Around the Law

To clarify, the Rolling Venture Funds is not a true “evergreen fund.” Rolling Venture Funds still need to comply with securities laws which prohibit venture capital funds from offering redemption rights to its LP base. The LPs's interests are illiquid until the fund is terminated- often a decade or more after it was formed, unless there are “extraordinary circumstances” (e.g., a death or bankruptcy).

In addition, each fund must comply with the Investment Company Act which requires:

Accredited Investors—Section 3(c)(1):

$10M+ funds: No more than 100 holders of LP interests if there is a mix of accredited investors and are “qualified purchasers” (note: non-accredited investors cannot invest in funds)

<$10M+ funds: No more than 250 holders of LP interests if <$10 million fund size.

Qualified Purchasers + Parallel Fund Structure—Section 3(c)(1) + Section 3(c)(7):

No more than 1,999 holders of LP interests, if a parallel fund structure is created with two funds: (1) Main fund consisting only of “Qualified Purchasers” ($5M in investments for individuals, $25M if an institutional LP); (2) Accredited Investor only fund, limited to 100 holders of LP interests.

AngelList recently wrote a letter to the Securities and Exchange Commission (“SEC”) advocating the removal of restrictions of secondary sales. AngelList wants the no-redemption rights lifted so that equity holders can liquidate their holdings in startups & funds. I wouldn’t hold your breath on the SEC changing its rules overnight, but having multiple, discrete funds may make it easier to transfer and sell fund holdings on the secondary market.

Conclusion

In general, my thoughts echo what Leo Polovets, Sahil Lavingia and Cindy Bi said about the Rolling Venture Funds model. There is no legal opinion that clearly authorizes these structures, and there may be complications that are not immediately apparent, but the same is true when anyone tries a new and interesting legal product. As @Naval himself wrote:

“Everyone's making it up as they go along. Figure it out yourself, and do it."

And as for those who still dispute the legality of the Rolling Venture Funds model, @Naval has some choice words for you:

If you've already subscribed, thank you so much—I appreciate it! 🙏

Subscribing to the Law of VC newsletter is free and simple. 🙌

As always, if you'd like to drop me a note, you can email me at chris@harveyesq.com, reach me at my law firm’s website or find me on Twitter at @chrisharveyesq.

Thanks,

Chris Harvey