#15 Episode - Getting the Count Right

Understanding the Limits of Investment Company Act & Optimizing Your Fund Size

Key Takeaways: New SEC Accredited Investor rules go into effect today (12/8/2020). Knowledgeable Employees won’t count against a fund’s 100/250 LP limits. General Partners are Knowledgeable Employees. But to maximize the number of LPs, split a fund into two parallel funds separated by Section 3(c)(1) and Section 3(c)(7).

Last week, I ran a poll on LinkedIn and Twitter in which about 100 people responded.

My question was:

What are the investor limits of VC funds with accredited investors?

• 99 LPs

• 100 LPs

• Some Other Number

Here were the results from Twitter:

And here were the results from LinkedIn:

The vote was pretty uniform across both platforms:

99 LPs—Most people (54-59%) believe the law limits funds to 99 persons.

100 LPs—About 25% of responders thought the law limits funds to 100 LPs.

Other—Only about 20% of responders thought there were other limitations.

Rather than bury the lede, here’s my answer:

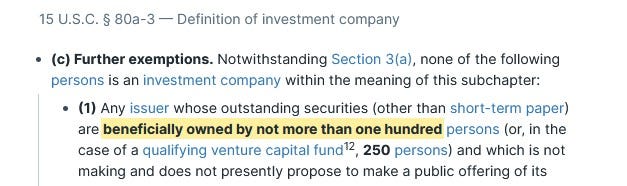

This is copied directly from the relevant statute under Section 3(c)(1) of the Investment Company Act—where does it say “99” LPs?

What Kind of Commitment Does It Take to Raise a VC Fund?

I’ll often see emerging managers try to raise $50M-$100M as their first venture fund.

“It’s better to risk boldness than triviality!” they might say.

Of course, fortune favors the bold. But in 2020, that needs to be tempered with reality. The average first fund size is $30 million, and that’s pre-pandemic. Having witnessed a fair number of emerging managers go through the LP fundraising gauntlet, it can be a humbling experience. This is true even for fund managers with good credentials.

For example, Elizabeth Yin at Hustle Fund said it took her and Eric Bahn over 9 months and 700 meetings with LPs before closing $11.5 million for their Fund I. (Elizabeth said she started only two months after giving birth to her younger child.)

The average fund closing was 18 months in 2019. In 2020, PitchBook Data indicates only 287 funds closed through 3rd Quarter in 2020, <50% from the totals of 2018.

That’s why Samir Kaji recommends first-time fund managers not be too strict with their initial closing numbers, even if it means reaching only 25-40% of your target fund size (but there should be a clear path to 50% of your target, particularly with Fund II+):

What are Your Minimum Commitments for LPs?

One of the first questions interested LPs will ask you is, “What are your minimums?”

Charlie O’Donnell, a GP at Brooklyn Bridge Ventures, had a great breakdown of the interplay between minimum LP commitments, target fund sizes and investment checks:

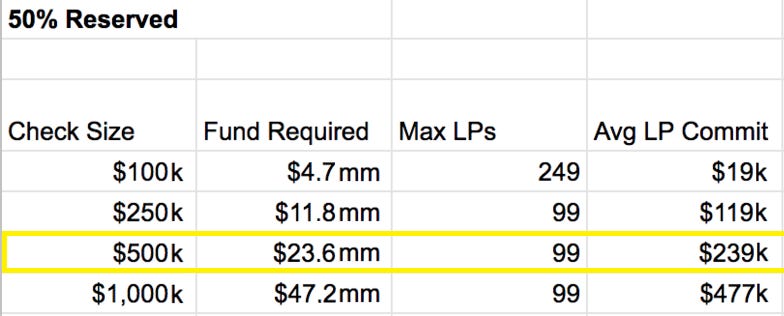

Let’s say you want to go raise a small seed fund. You’re not even looking to go big. You want to write $100k investment checks and be done with it. You can’t really lead rounds and you can’t support them over time. Here’s what it looks like in terms of raising from just “normal” wealthy people (Accredited Investors), assuming they’re not all super-wealthy (Qualified Purchasers or “QPs”).

In other words, if you plan to write $500k checks into your startups with 1:1 reserves, even with a fund size of $23.6 million, your average LP commitment must be at least $239k per investor. Very few people can hit that kind of hurdle and you only have a certain number of slots available—which explains why average minimums are so high:

TinySeed, a venture-like fund, believes these arbitrary numbers should change:

The current limit of accredited investors [in venture funds] hurts capital formation, reduces investment opportunities, increases the risk to individual investors and decreases access to private capital markets for underrepresented groups.

Framework for Venture Capital Fund Law

Before we jump into the law, a fair warning:

The relevant fund law was drafted in the 1930s & ‘40s during the Great Depression, so the language, structure and definitions are just like reading an Old English book. Difficult to parse. Difficult to understand. Difficult to even explain it.

But as Jeff Morris Jr. recently wrote:

Reading Substack newsletters is adult homework.

So—buckle up, put on your reading glasses, and let’s get to work.

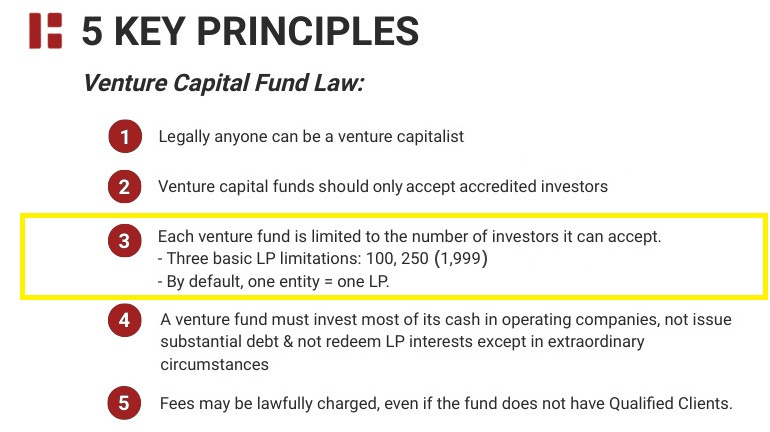

In Law of VC - Episode #11, we went over the five principles of venture capital fund law:

Limitations of Investors for Each Venture Fund:

“100, 250 (1,999)” refers to the following:

100 / 250: Section 3(c)(1)—any Accredited Investors* in the fund; and

1,999**: Section 3(c)(7)—Qualified Purchasers (QPs) only.

*We defined Qualified Purchasers and Accredited Investors in Law of VC Ep. #11, but they are now contained in my Roam Research database (link).

**1,999 is not an actual limit but more of a practical one as Section 12(g) of the Exchange Act of 1934 requires public registration at 2,000+ holders.

99 Investor Problem: The Prevailing View of the VC Industry

The 99 investor limit has been the prevailing view of the venture industry for decades.

In 1996, Congress passed the National Securities Market Improvements Act of 1996 (“NSMIA”) which split the law into two sections: Sections 3(c)(1) and 3(c)(7). 3(c)(1) is intended for all investors while 3(c)(7) is for Qualified Purchasers only.

In 2018, Congress passed an amendment to Section 3(c)(1) so VCs could add 250 LPs to the fund, but limited the total amount to $10 million.

Note: This didn’t completely solve the “99 Investor Problem,” but it gave an opportunity for more investors to participate in ≤$10m (MicroVC) funds.

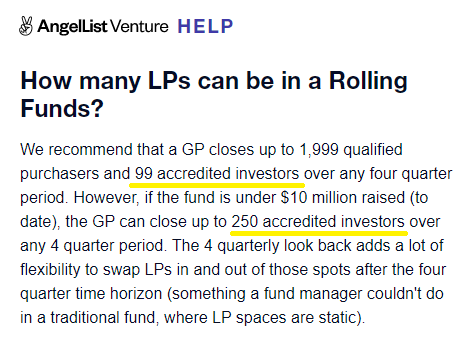

In 2020, AngelList launched Rolling Venture Funds (see Law of VC Ep. #2). Interestingly, Rolling Funds may reset their accredited investor limits each year, due to the fact that each fund is a separate series (funds can be integrated if a reasonable investor would consider the interests not to be materially different):

Essentially, the reason that the VC industry has viewed funds as limited to 99 persons as opposed to 100 persons is because it was assumed the general partner’s (“GP’s”) commitment counts as one of the 100 investors, which means the effective number of permitted investors was 99. The “99 Investor Problem” became part of the lexicon.

Before the NSMIA passed in 1996, fund managers argued their interests did not count towards the 100 investor limit because the GP commit was not a security. The SEC accepted that interpretation (see SEC No-Action Letters, Colony Realty Partners 1986, L.P.; see also Shoreline Fund, L.P. 1994).

Side Note: A general partner’s interest may be considered a security if the GP has no meaningful stake or has no involvement in the venture fund itself. Under the Howey Test, the “efforts of third parties” is one prong resulting in an investment contract being deemed a security. Whether a GP can be considered a “third party” to the fund rather than a participant or manager of the fund, is a fact-based inquiry based on their involvement in the operations of the fund.

Therefore, it was assumed, so long as the GP’s interest would not constitute a security, there would be 100 slots available, not 99. But as a precautionary measure, the VC industry opted to use “99” as a heuristic. Better to be safe than sorry!

100 Investor Problem: Knowledgeable Employees Excluded

Today, December 8th, 2020, the SEC will add new categories to the Accredited Investor rules to enable funds to raise from what used to be considered non-accredited investors. Knowledgeable Employees will qualify as Accredited Investors.

Here’s the legal definition:

So, in other words, Knowledgeable Employees are (i) general partners, directors, etc. (including managing members), and (ii) employees who are involved in the investment activities of the fund who have at least one year of similar experience under their belts.

Some lawyers might quibble with whether a managing director can be a “Knowledgeable Employee” if that person is not a W2 employee, but as all tax lawyers know, a member cannot be a W2 employee and an owner of a limited liability company.

Now, here’s the interesting part — Rule 3c-5(b) excludes not only “Knowledgeable Employees” (which must be ‘natural persons’) but also any company owned exclusively by Knowledgeable Employees — see the highlighted text below in Rule 3c-5(b)(2):

Here’s why investor limits should be 100 and not 99:

To summarize what this ultimately means:

Key Takeaway: Knowledgeable Employees won’t count against your fund’s 100/250 LP limits under Section 3(c)(1) of the Investment Company Act. And GPs are considered Knowledgeable Employees.

Final Count

Of course, one investor does not make a huge impact. As one GP recently told me, “So What?” It’s kind of like increasing the speed limit from 60mph to 65mph. Not going to change a whole lot.

But the pearls of wisdom lie here:

You can have a venture fund with more than 100 investors, provided you separate qualified purchasers from your accredited investors. For example, Motley Fool has a venture fund with over 800 limited partners in it.

The trick is to open a parallel fund with qualified purchasers only and keep all of your accredited investors housed under the Section 3(c)(1) fund. If structured like that—Section 3(c)(1) vs. Section 3(c)(7)—the SEC will not “integrate” the funds and you can have as many Qualified Purchasers and as many Knowledgeable Employees as you’d like (with a practical limit of 1,999 before being required to publicly register) plus an up to an additional 100 Accredited Investors.

Subscribing to the Law of VC newsletter is free and simple. 🙌

If you've already subscribed, thank you so much—I appreciate it! 🙏

As always, if you'd like to drop me a note, you can email me at chris@harveyesq.com, reach me at my law firm’s website or find me on Twitter at @chrisharveyesq.

Thanks,

Chris Harvey