#13 Episode - New Rules for Equity Crowdfunding

Equity Crowdfunding is Not Competing with Venture Capital, But It May Fundamentally Change the Investing Landscape for 87%+ of Americans

On November 2, 2020, the day before the U.S. Presidential Election, there were some big announcements on equity crowdfunding from the Securities and Exchange Commission (“SEC”) that got lost in the shuffle.

Today, March 15th, 2021, those same SEC equity crowdfunding rules go into effect.1

Key Takeaways:

Regulation Crowdfunding annual limits moved from ~$1 million to $5 million

Regulation A annual limits increased from $50 million to $75 million

Some other improvements will make it easier to raise via equity crowdfunding

Equity crowdfunding might finally live up to its promise of disrupting early-stage financing. But will it actually compete with venture capital?

As Tyler Tringas framed the issue:

Every venture capitalist knows that the keys to a successful fund portfolio are access and deal flow. The venture capital industry is a zero-sum game built on a heavy-tailed power law distributions. Signal, brand, and exclusivity mean everything to a VC.

Crowdfunding is the opposite. There are inherent network effects in crowdfunding. The more investors that join an equity-crowdfunded offering, the better. What matters to crowdfunded investors is community, transparency, and participation.

The crowd wants businesses that are (1) profitable, (2) small-to-medium sized (SMBs), and (3) mission-driven or impact-focused. Historically, those businesses were exactly what VCs avoided.

Old Power vs. New Power

The power dynamic between VC and crowdfunding is “Old Power” vs. “New Power”:

While Old Power is jealously guarded by the few, New Power is promoted by the many. Old Power rests on governance, authority, and exclusivity. New Power is about collaboration, radical transparency and community values.

Those same power dynamics are at play here:

Crowdfunding

Crowdfunding grew in substantial popularity due to the Internet. It has enabled entirely new industries. Generally speaking, crowdfunding is made up of five categories:

Rewards (Kickstarter, Indiegogo)

Donations (GoFundMe)

Debt (Lending Club)

Assets (Real Estate, Fine Art)

Equity crowdfunding (AngelList, Republic, Wefunder)

1. Equity Crowdfunding

Unlike other types of crowdfunding, equity crowdfunding is regulated by the SEC. Basically, there are three securities laws that apply to equity crowdfunding:

Regulation D

Regulation A

Regulation Crowdfunding (“Reg CF”)—the purest form of equity crowdfunding

All three securities laws permit investments from non-accredited investors, which are people who make up roughly 87% of the population of US households (Accredited investors have been previously discussed on Law of VC Episodes #5 and #11).

The relevant question is whether general solicitation is allowed and, if so, the extent to which non-accredited investors are entitled to participate in the offering.

2. JOBS Act of 2012

The three securities laws above formed the backbone of the Jumpstart Our Business Startups (JOBS) Act of 2012. The purpose of the JOBS Act was to create jobs by allowing small and mid-sized businesses to crowdfund their capital financing needs. Since 1933, equity crowdfunding required a company to register to go public if it was selling securities to the public. That ban was partially lifted by the JOBS Act.

(i) Regulation D

Without a doubt, the most transformative rule change of the JOBS Act was Rule 506 of Regulation D. The law split Rule 506 into two exemptions: Rule 506(b) & 506(c).

Rule 506(b) was largely a copy of the same rule already in play. Rule 506(b) does not permit general solicitation but it allows up to 35 non-accrediteds.

Rule 506(c) allows general solicitation, but does NOT allow non-accrediteds. Importantly, startups & funds can raise an unlimited amount of money provided that the issuer (the startup or fund) takes reasonable steps to verify the accredited investor status of each investor.

Rule 506(c) was directly responsible for new business models such as AngelList’s Syndicates, Rolling Venture Funds and AngelList’s Access Fund.

While Rule 506(c) locked out non-accredited investors from participating in new startup investment opportunities, it didn’t actually change the game. For example, from 2009-2019, only between 3.4%-6.9% of Rule 506 offerings included non-accredited investors [FN1]. And if every self-prepared LP investor questionnaire is to be believed as true and accurate, ~0% of non-accredited investors have participated in venture capital funds [FN2—Law of VC #11, “VC funds should only accept accredited investors”].

(ii) Regulation A

Regulation A (or Regulation A+) is a unique offering exemption that provides startups with a pathway to go public with some training wheels. The description most people use is that it’s a “mini-public offering.”

Regulation A+ has two tiers:

Tier 1, for offerings of up to $20 million in a 12-month period; and

Tier 2, for offerings of up to $75 million in a 12-month period (most common).

Regulation A is similar to an S-1 registered offering, but with a lot less work & stress.

The offerings are made public and can be sold to non-accredited investors. But the company does not need to list on a public stock exchange and it can “test the waters” to gauge investor interest before launching.

Regulation A is an interesting exemption but no breakout startup has yet to successfully use it. Elio Motors, a car manufacturer, was perhaps the most famous company to use it out of the gate. But since the company announced its intent to sell “ElioCoins” in 2018, it seems to have flamed out.

Regulation A looks promising to the real estate crowdfunding market. Not many startups have successfully used it. That being said, $75 million per year is a lot of money for some ambitious founders looking to capitalize on private dollars outside of VC.

(iii) Regulation Crowdfunding (Reg CF)

On May 16, 2016, four years after the JOBS Act passed, equity crowdfunding rules finally went into effect. That same day, I wrote an article about it: “Equity Crowdfunding Finally Goes Into Effect Today, but Is the New Law Worth It?”

My conclusion was that Reg CF wasn’t worth it for VC-backed startups. The original law had six fundamental problems with it:

$1 million cap per year was too small

The costs of compliance too high

Messy cap tables (no SPVs allowed)

Very limited advertising or solicitations allowed

No testing the waters

Lack of any secondary market

The new rules attempt to solve some of the issues that plagued this law by:

Allowing SPVs, which should reduce the forced practice of some platforms to have “lead investors” with a mandatory 10% carried interest thrust onto investors

Relaxing rules to permit “test-the-waters” and “demo day” activities are nice, but they will likely have a very small impact on startup fundraising activities

Reducing time periods between fundraises to minimize “integration” issues—again, nice, but hard to tell how much that changes the impact of fundraising

On the investor side in 2021, accredited investors will have no investment limits under Reg CF. A recent study found that typically 80% of the investors are accredited and 20% are non-accredited, so this is welcome news for startups.

Overall Analysis

Even though the changes to the equity crowdfunding laws are nice, they will not open the floodgates so venture capital has to worry about it.

Perhaps the biggest weakness of the Reg CF rules is startups are forced to raise in only one location: Crowdfunding portals registered by the SEC and regulated by FINRA. No rule change is going to change that foundational impediment. That seems to have been by design.

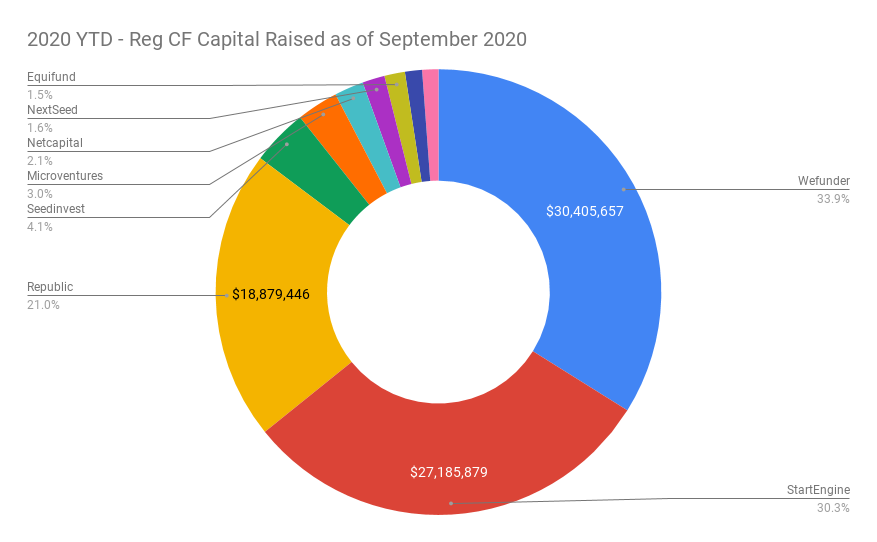

Here’s a graph that shows the impact of the various securities exemptions:

The most revealing finding above is that equity crowdfunding had no impact on how VC funds and VC-backed startups have raised funds.

Rule 506(c), the most important law change of the JOBS Act, was only responsible for 4.2% of the fundraising activity under Rule 506 offers during the year of 2019.

Things may change post-pandemic, along with recent SEC rule changes on accredited investors, equity crowdfunding, and other improvements to the rules. But it will be some years, maybe even decades, before startups that advertise their offerings online outpace those startups who don’t advertise their offerings.

The second weakest reason to use equity crowdfunding has to do with reporting. After you close your first round, each year you need to make a public filing with the SEC that discloses certain key information, including financials. The Form C-AR, as it’s called, requires disclosures substantially similar to the disclosures provided in the “Form C,” except you do not need to discuss securities being sold. You must provide GAAP financials for the next fiscal year not previously disclosed; however, these do not need to be reviewed or audited. You are required to present reviewed or audited financial statements only if you have had this done since the campaign ended. Otherwise the financial statements must be certified by the CEO.

This requirement is only terminated when:

You become a public reporting company (i.e., you “go public”);

you’ve made a Form C-AR filing already and have less than 300 holders of record;

you’ve filed 3 Form C-ARs and have total assets that do not exceed $10,000,000;

you repurchased all outstanding securities issued through the Reg. CF platform; or

you liquidate or dissolve your business in accordance with state law.

The rule changes did not modify this requirement.

Even after the recent equity crowdfunding rule changes, there are two fundamental reasons why equity crowdfunding will not compete with or outpace venture capital:

First, there isn’t enough money in the equity crowdfunding ecosystem. Venture capital is a $450+ billion AUM asset class supported by institutional players like pension plans, foundations, endowments, sovereign wealth funds, and corporate venture interests.

In 2019, the VC industry invested $136.5 billion in US-based private companies and will reach at least $100+ billion for 2020.

Equity crowdfunding (Reg CF) raised ~$400M over the span of 4 years.

Although equity crowdfunding campaign numbers are up significantly since the start of the pandemic, VC is 1,000x+ larger than what the equity crowdfunding industry is today for startups.

Second, there is no easy way for equity crowdfunding investors to get their money out. Equity crowdfunding was never intended to have a robust secondary market. But for high-growth, VC-backed startups, highly compensated exits are a must. Silicon Valley has a fail-first mentality because the relatively few VC-backed startups that make it return vast amounts of cash. When liquidity exits are uncertain or not there, the market cannot be expected to grow.

Conclusion

Many VCs think equity crowdfunding has failed to live up to its promises. But they're looking at it over a very short time period. If you judged the VC market in the 1950s to the early-1990s—people would have concluded the same thing: A dead asset class. Equity crowdfunding has only been around for a few years.

I have no doubt that the equity crowdfunding market will accrue to a greater market cap than where VC is today. The only question is timing—when will societal and regulatory changes catch-up to the kind of growth that we expect to see in the coming years? Within the next 10 years, or as many years as it took venture capital to get where the VC industry is at today?

For 87% of Americans who are non-accredited investors, the hope of equity crowdfunding is that it will provide them with the opportunity to increase their wealth as much as private startup investing has increased the wealth of accredited investors.

Subscribing to the Law of VC newsletter is free and simple. 🙌

If you've already subscribed, thank you so much—I appreciate it! 🙏

As always, if you'd like to drop me a note, you can email me at chris@harveyesq.com, reach me at my law firm’s website or find me on Twitter at @chrisharveyesq.

Thanks,

Chris Harvey

This article has been edited from November 15, 2020. See SEC Final Rule for Regulation Crowdfunding (Nov. 2, 2020); see alsoSEC Harmonizes and Improves “Patchwork” Exempt Offering Framework.